Executive Summary

- The town hall expanded the case for HIP 149: Mario Di Dio and the Helium team framed the proposal as a way to resource carrier growth, retire Proof of Coverage as the main reward signal, add deployer downside protection, and keep oversight tied to HNT governance.

- The carrier thesis centered on Wi-Fi offload demand: Speakers argued that 5G and 6G capex pressure, direct-to-cell satellite limits, and fixed wireless capacity needs make indoor Wi-Fi offload more valuable over the next several years.

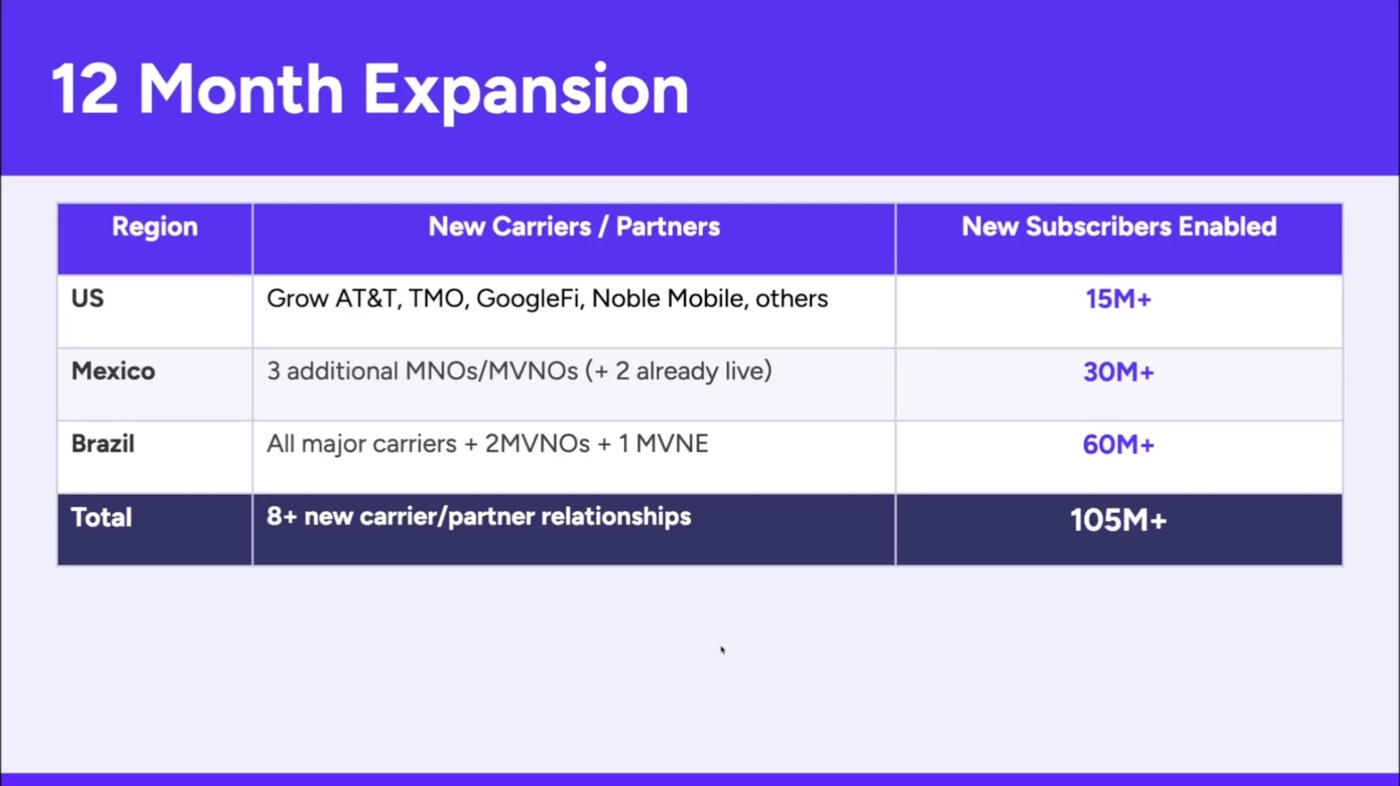

- The slides gave a 12-month expansion target: The team presented a bull-case plan for 8+ new carrier or partner relationships and 105M+ new subscribers enabled for Helium offload across the US, Mexico, and Brazil. Speakers stressed that telecom sales cycles are long and that this is a pipeline case, not a guarantee.

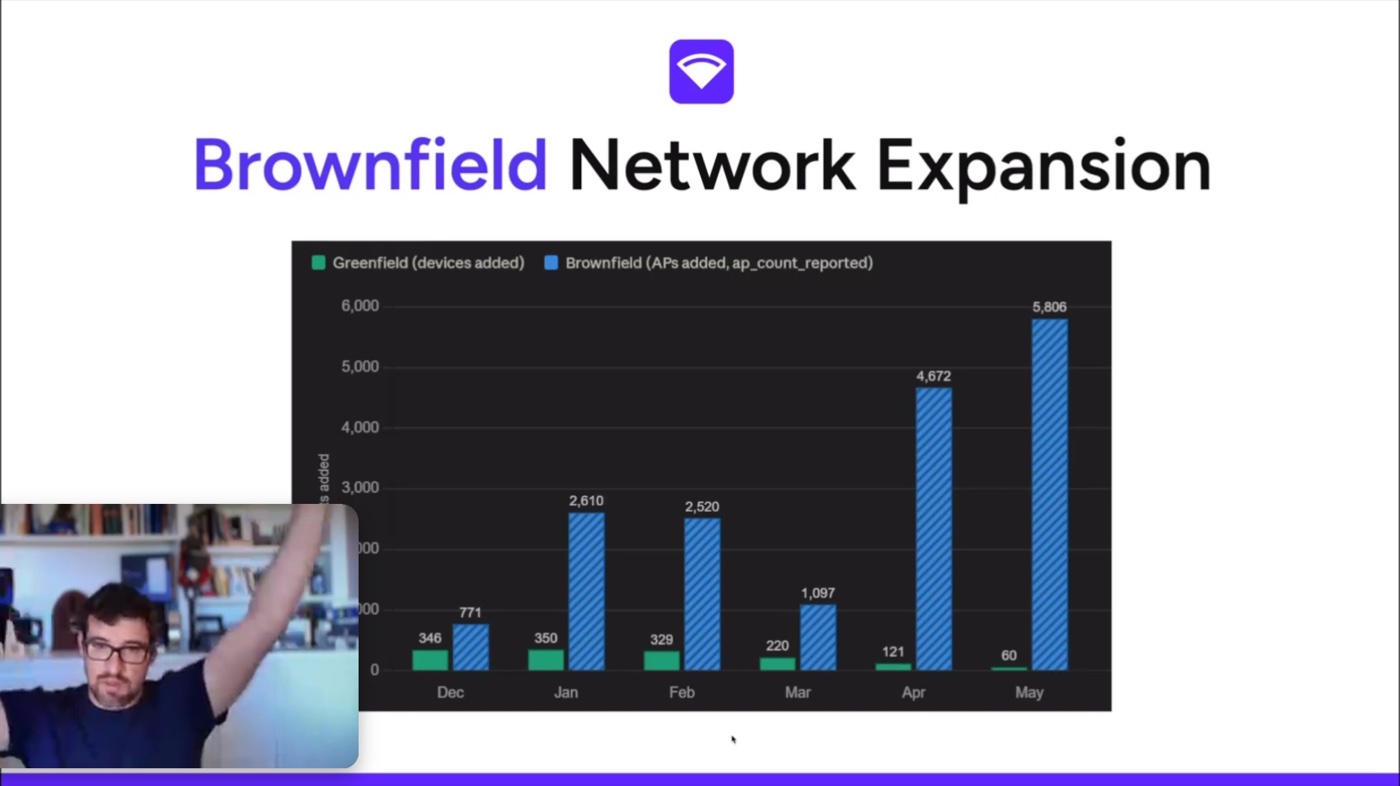

- Brownfield deployments were presented as the near-term growth engine: The deck showed almost 6,000 access points added in May, roughly 15.3k brownfield units in the pipeline as of June 9, and a US carrier request to cover about 30,000 locations.

- The product roadmap is meant to make offload easier for carriers and deployers: The team discussed AI and network data, Passpoint tooling, quality-based offload controls, MVNE carrier enablement, expansion zones, auto reward splits, advanced analysis, and a consolidated deployer experience.

- The Q&A focused on trust, transparency, and economics: Questions covered stalled visible metrics, Nova financial transparency, why protocol resources are not Nova equity, network operating costs, offload rates, international expansion, equipment subsidies, and whether future HNT emissions can be permanently capped.

What Happened

The event opened as a follow-up to the earlier Helium proposal discussions. Scott said the team wanted to address community questions around network vision, use of funds, accountability, and the details behind the proposal before the vote. Mario Di Dio then introduced the presentation as an attempt to explain both the long-term industrial case and the next three to six months of product and growth work.

Carrier Demand Thesis

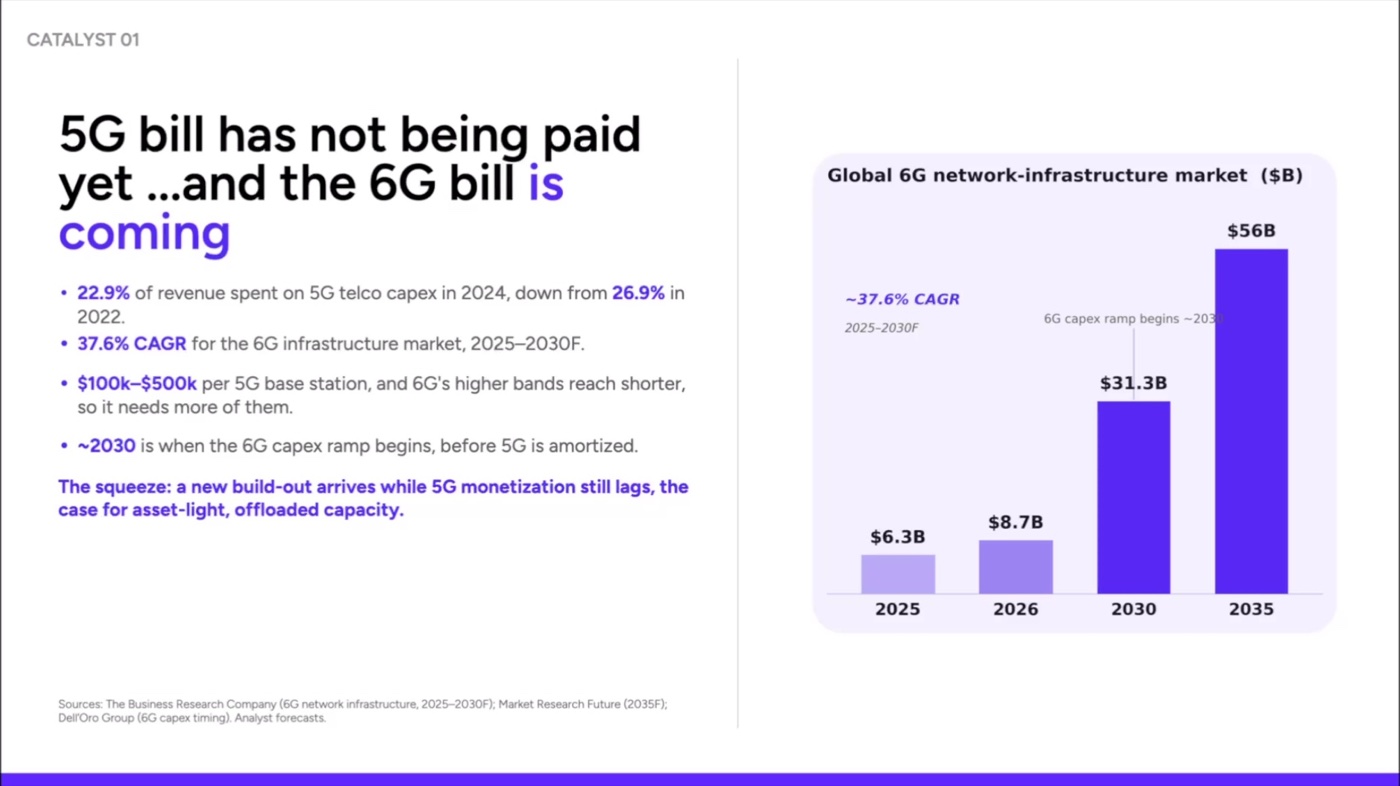

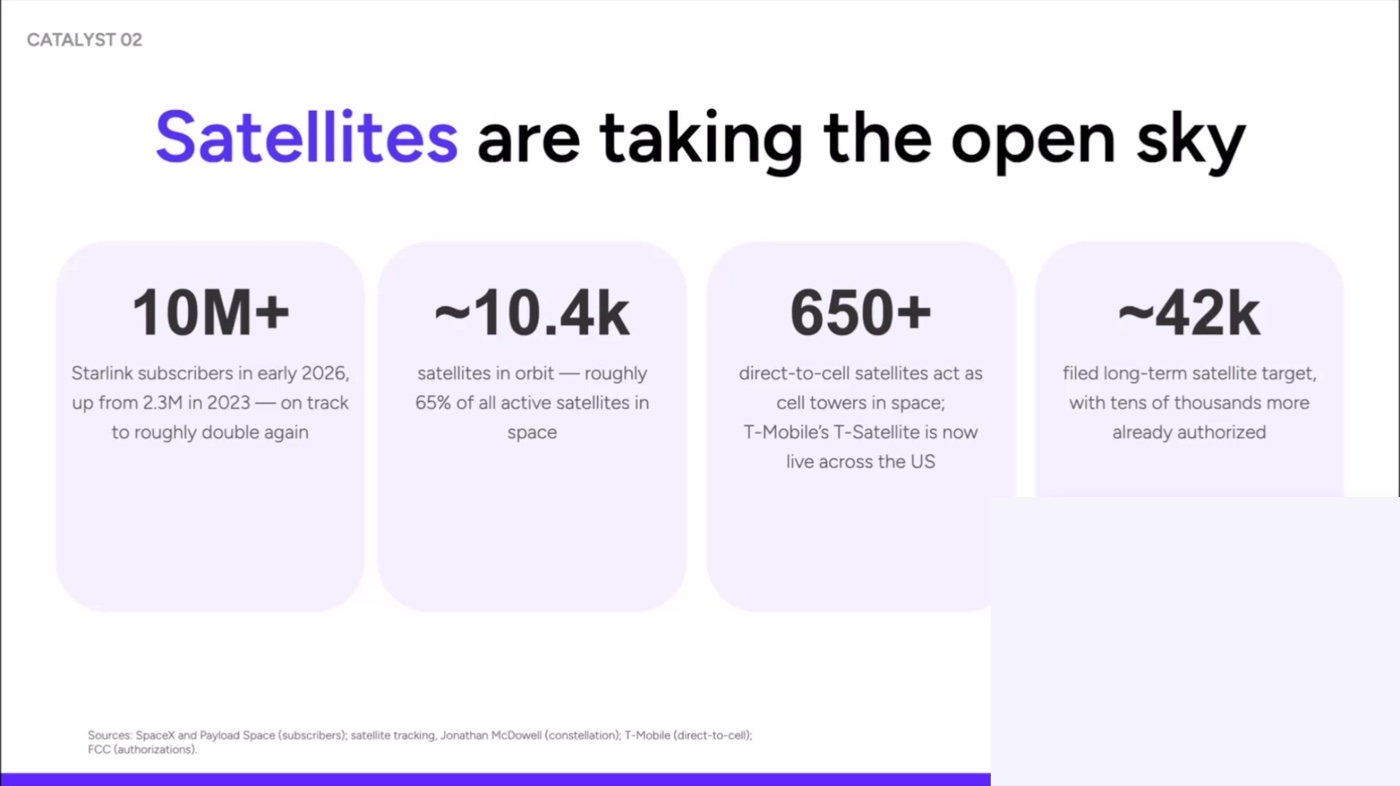

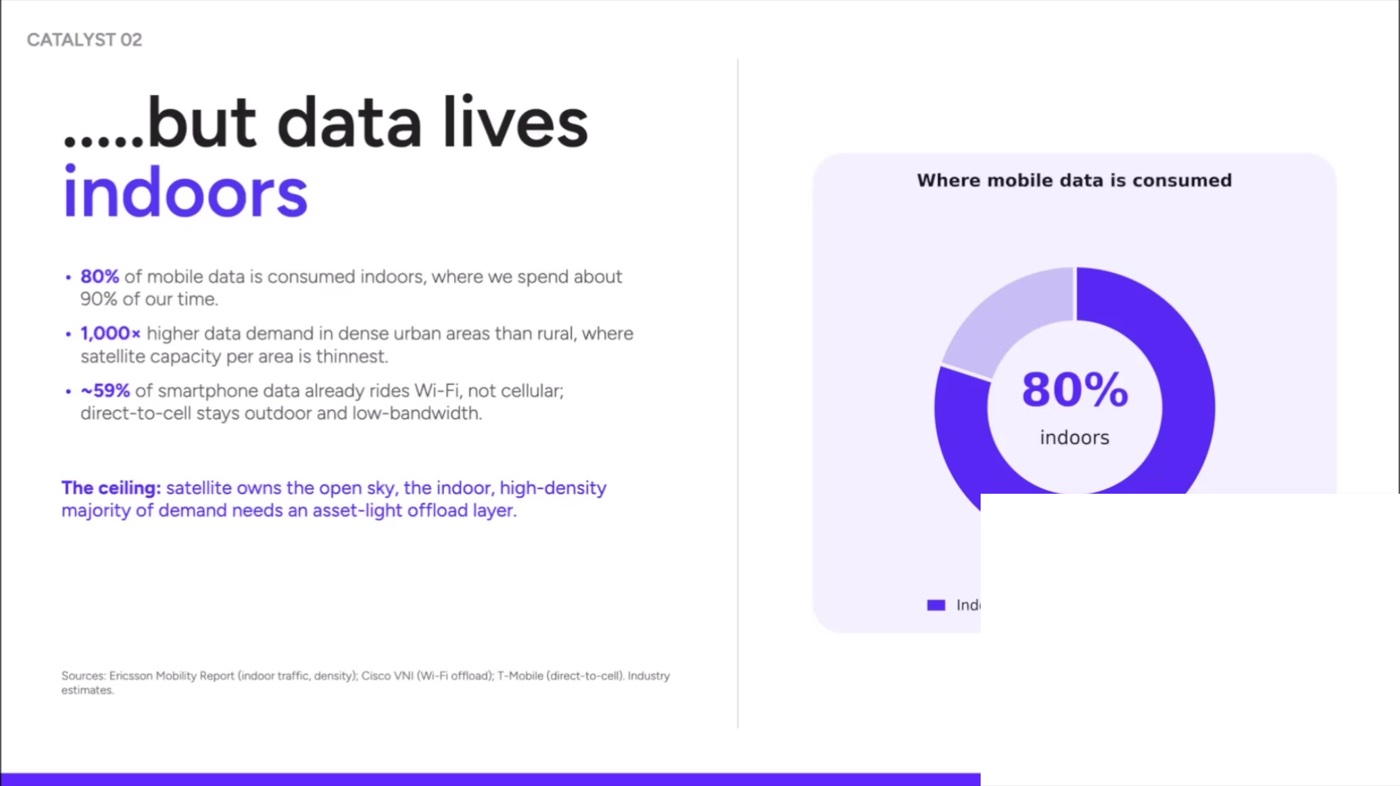

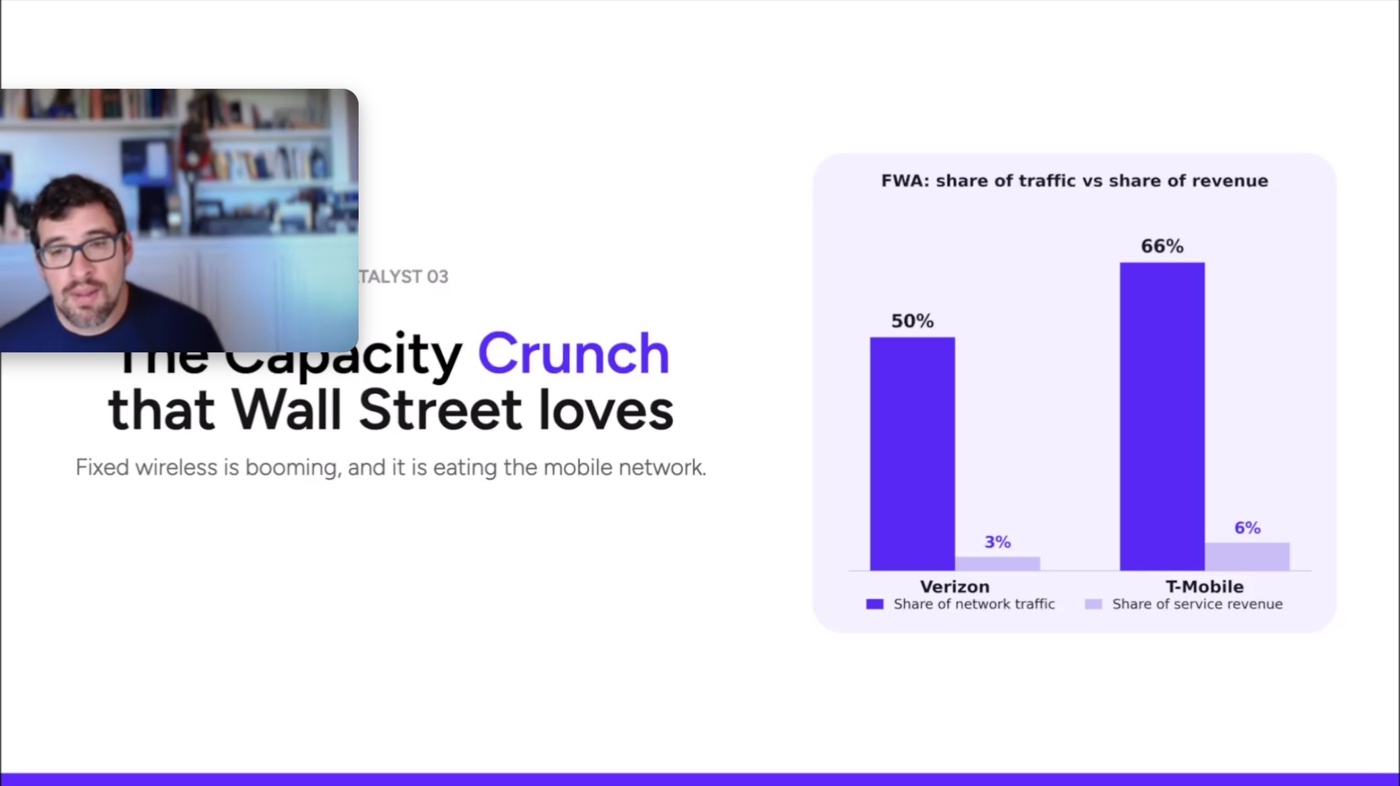

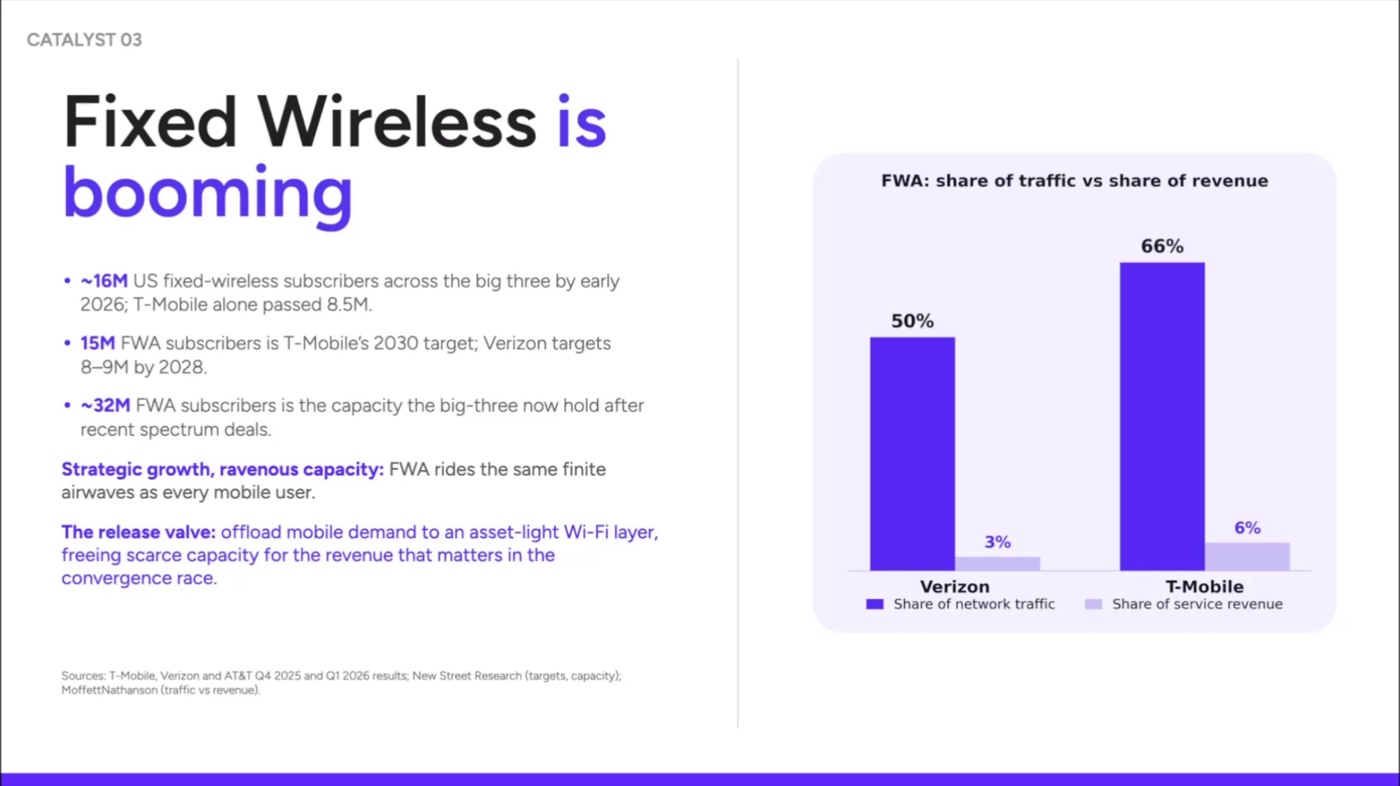

Mario argued that Helium's value should increase if carriers are pushed toward asset-light ways to add capacity. He described three pressures driving that view. First, carriers are still working through 5G investment while the 6G capex cycle is already approaching. Second, direct-to-cell satellites can help with outdoor coverage but cannot serve most indoor mobile data demand. Third, fixed wireless access is growing because carriers use it to compete with cable and fiber, but it consumes large amounts of cellular capacity.

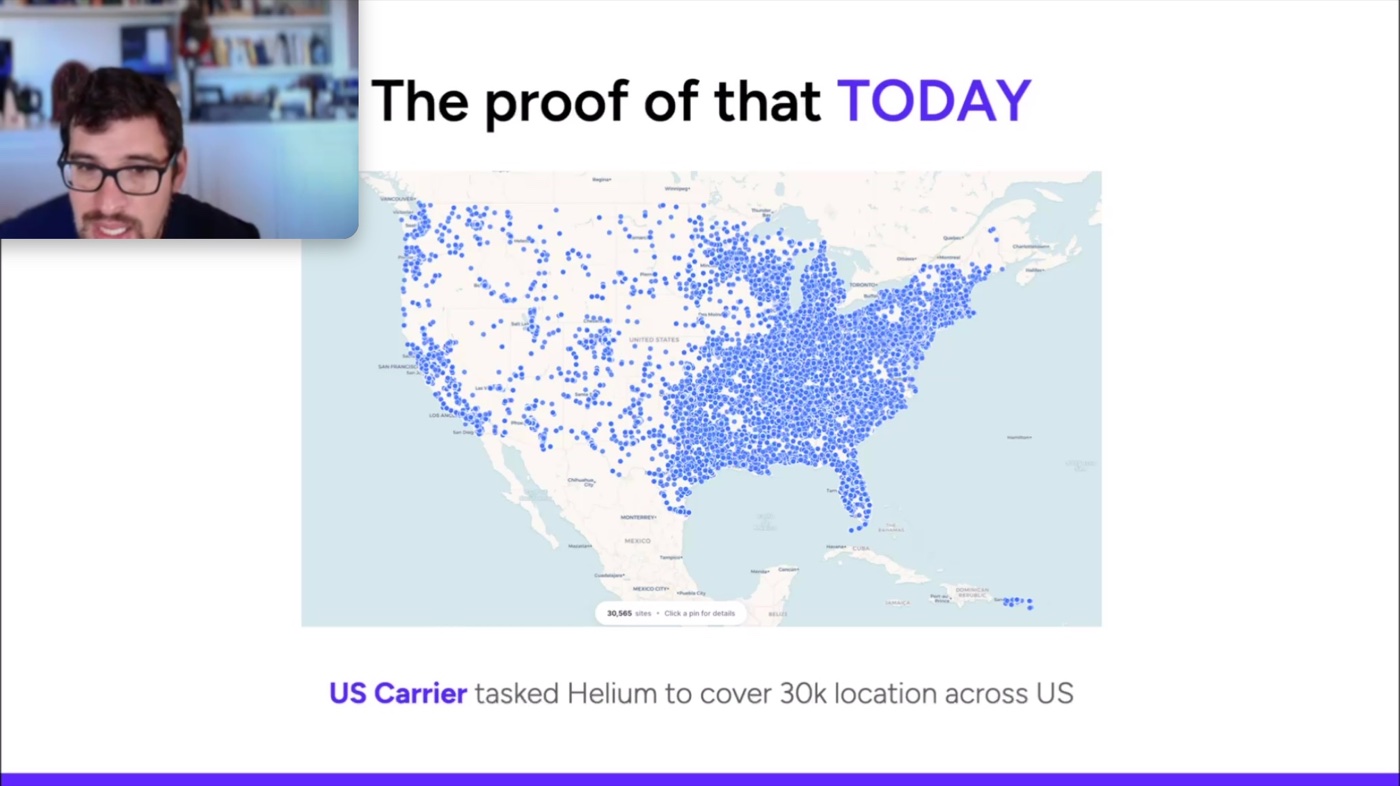

The conclusion was that carriers need cheaper ways to move indoor mobile traffic off constrained cellular networks. The presentation positioned Helium's community-built Wi-Fi footprint as a way to do that without carriers directly owning every site. The team cited one US carrier request for Helium to help cover more than 30,000 locations as evidence that the demand is already visible.

Proposal Mechanics

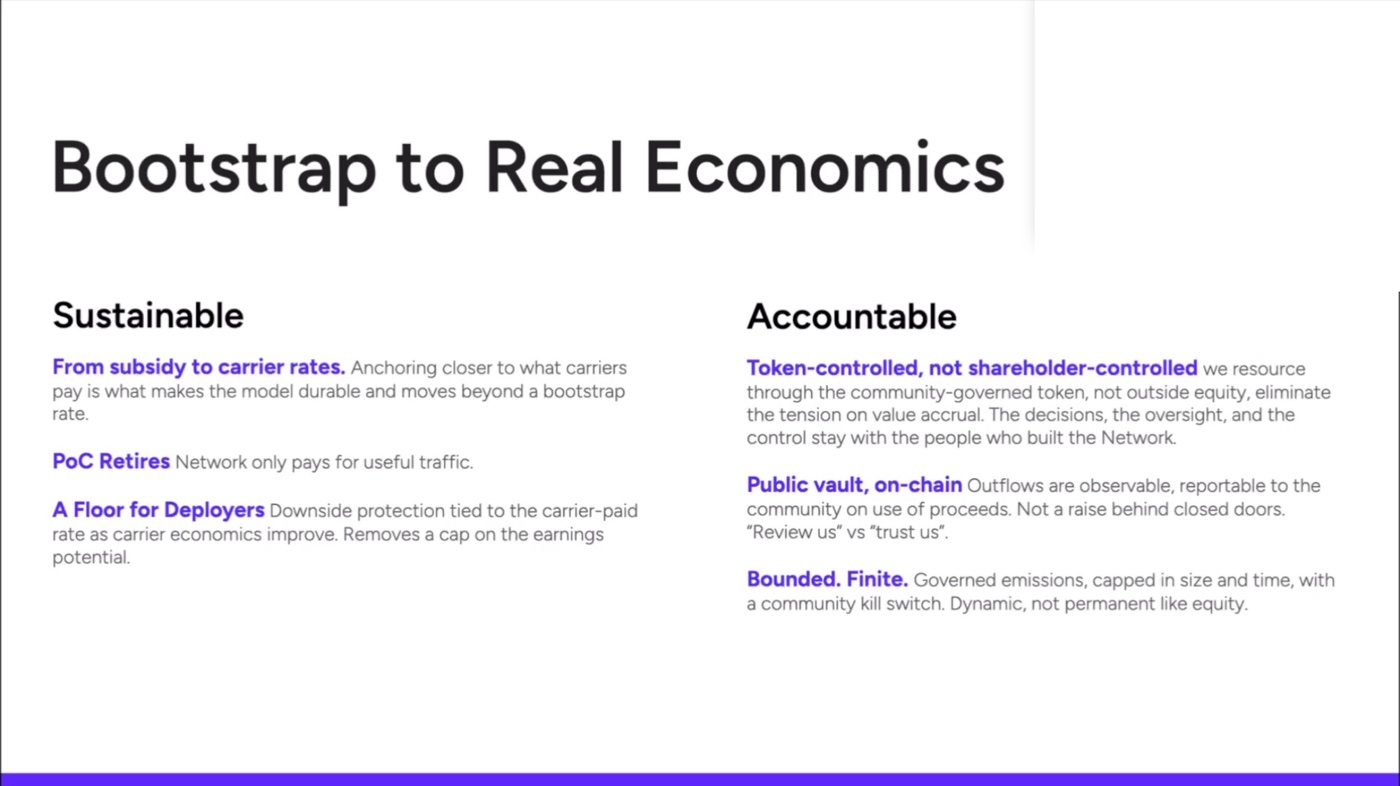

The discussion tied this demand thesis back to HIP 149 and the related Helium Mobile transition. Speakers said the proposal is meant to move the network from bootstrap rewards toward real carrier economics. In that framing, Proof of Coverage retires as the main growth mechanism, useful traffic becomes more important, and deployers receive a floor intended to protect downside while preserving upside if traffic and rates improve.

Mario emphasized that the proposed resources would be token-controlled rather than shareholder-controlled. He described the on-chain vault, community governance, and advisory council as the accountability structure. He also said Nova would vote because it is a major stakeholder, while arguing that the company does not have enough votes to pass the proposal alone.

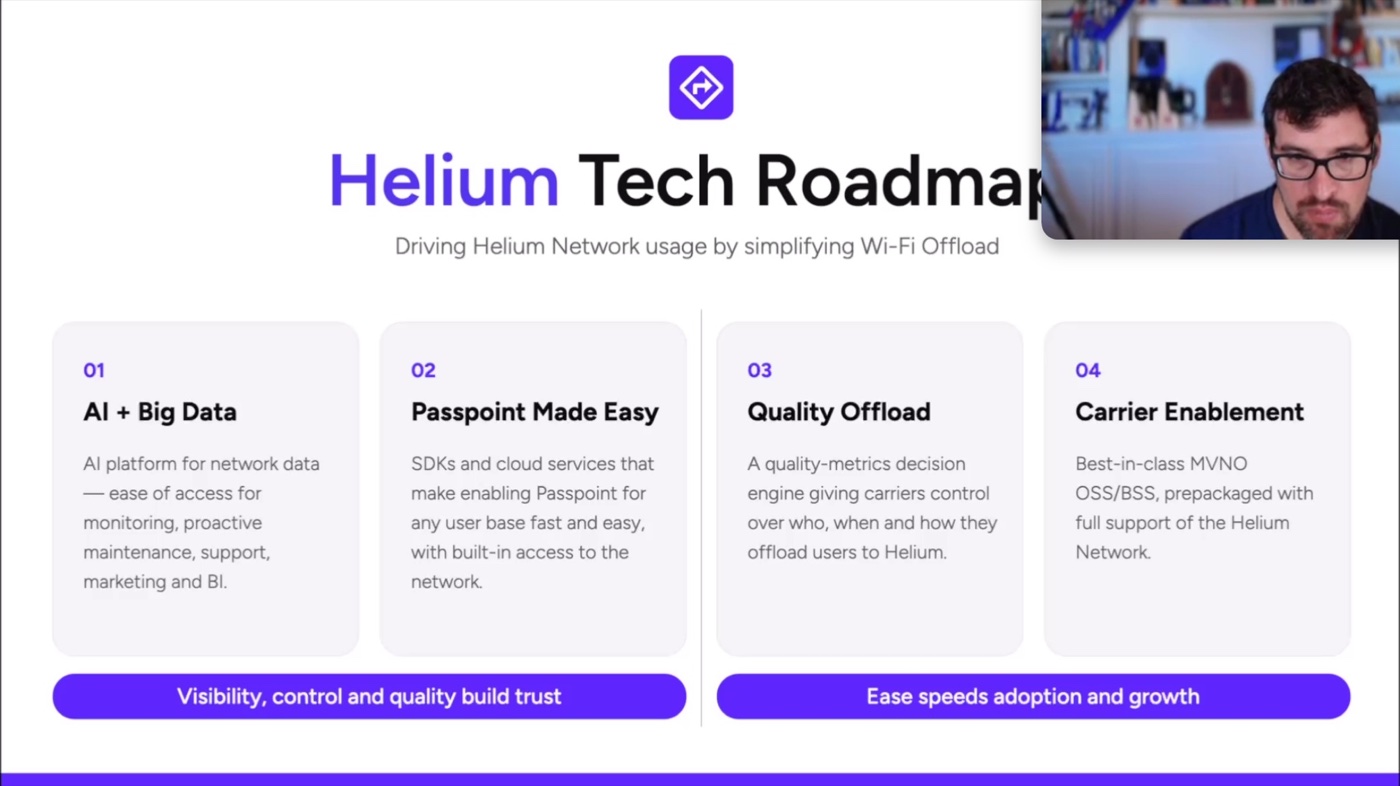

Technology Roadmap

Joey Padden described the technical roadmap as two related goals: building carrier trust and making carrier onboarding easier. The roadmap included an AI and big-data platform for network visibility, quality metrics that help carriers decide when and how to offload users, SDKs and cloud services for Passpoint enablement, and an MVNO backend with Helium Network offload support built in.

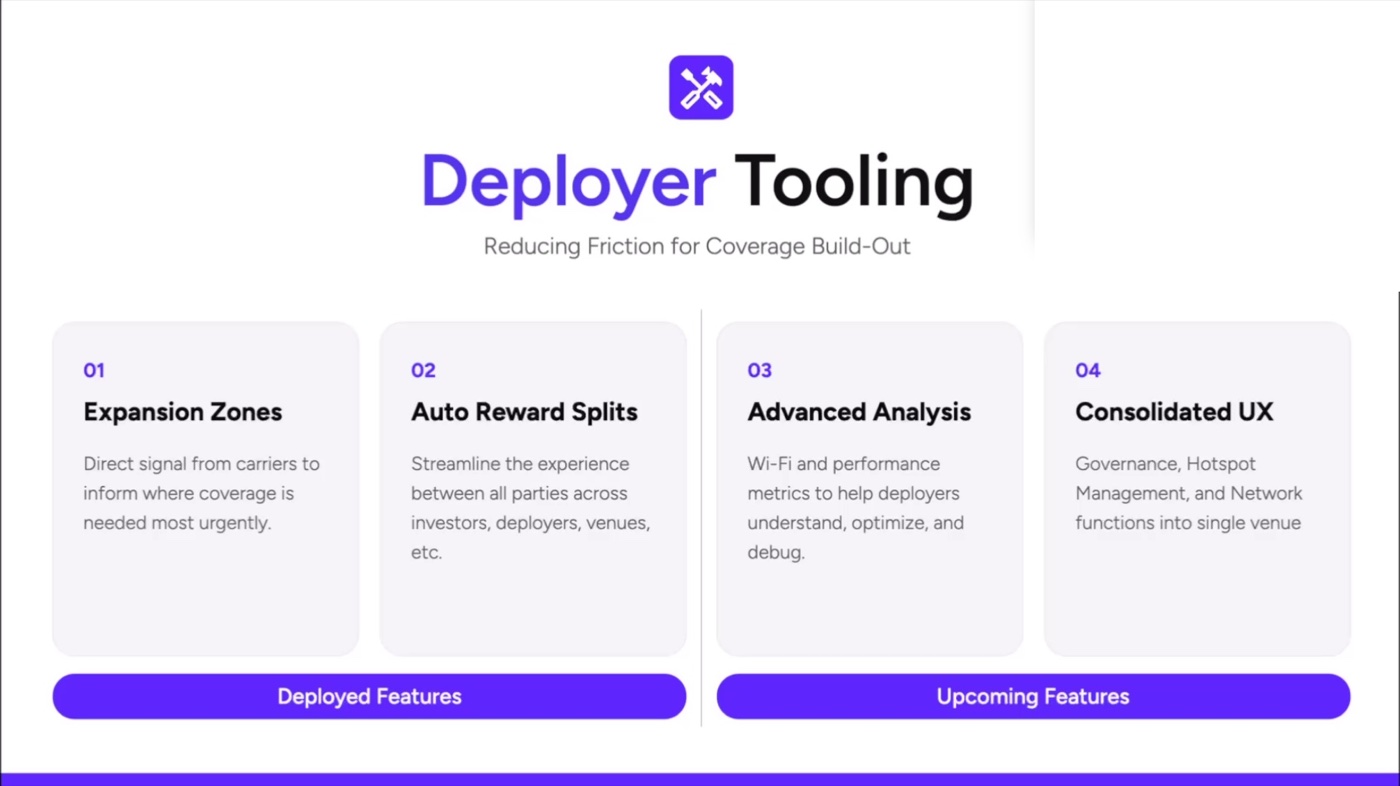

The deployer tooling section focused on reducing friction for coverage build-out. The team highlighted expansion zones as direct carrier signals for where coverage is needed, auto reward splits for venue or business-owner partnerships, upcoming Wi-Fi performance analysis for deployers, and a consolidated experience for governance, hotspot management, and network functions.

Brownfield Network Expansion

Woody Schneider described brownfield deployments as taking existing network infrastructure and joining it to Helium. He said recent growth is overwhelmingly coming from brownfield because these deals are driven first by venue coverage needs and only secondarily by hotspot earnings. The slide deck showed 5,806 brownfield access points added in May and a pipeline snapshot with 61 records, 15,324 total brownfield units, and 15,366 total units in pipe as of June 9, 2026.

Speakers cautioned that signed and joined brownfield locations do not all carry traffic immediately. They said activation can happen in stages, so data transfer and daily-active-user metrics may lag behind signed coverage.

Carrier Expansion Plan

Mark Phillips said the US remains the core market while Mexico and Brazil are the two named expansion markets. He framed offload as the wedge into larger multi-product relationships, where Helium's software and services stack can sit on top of offload. The team said it is not interested in entering a new geography just to build speculative coverage; they want a local partner and carriers ready to do deals.

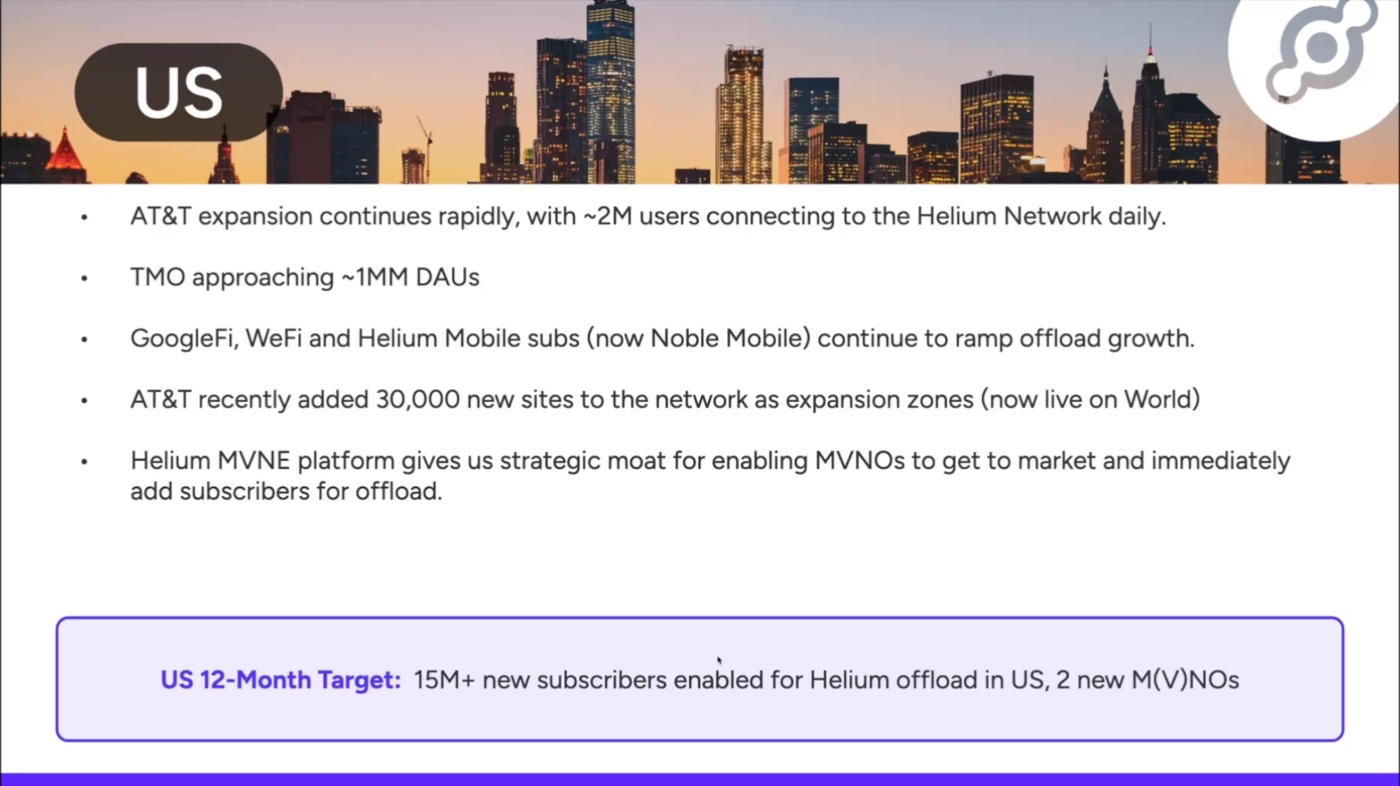

For the US, the slides said AT&T expansion continues rapidly with about 2M users connecting to the Helium Network daily, T-Mobile is approaching about 1M daily active users, Google Fi, WeFi, and Noble Mobile continue to ramp offload growth, and AT&T recently added 30,000 expansion-zone sites. The US 12-month target was 15M+ new subscribers enabled for Helium offload and two new M(V)NOs.

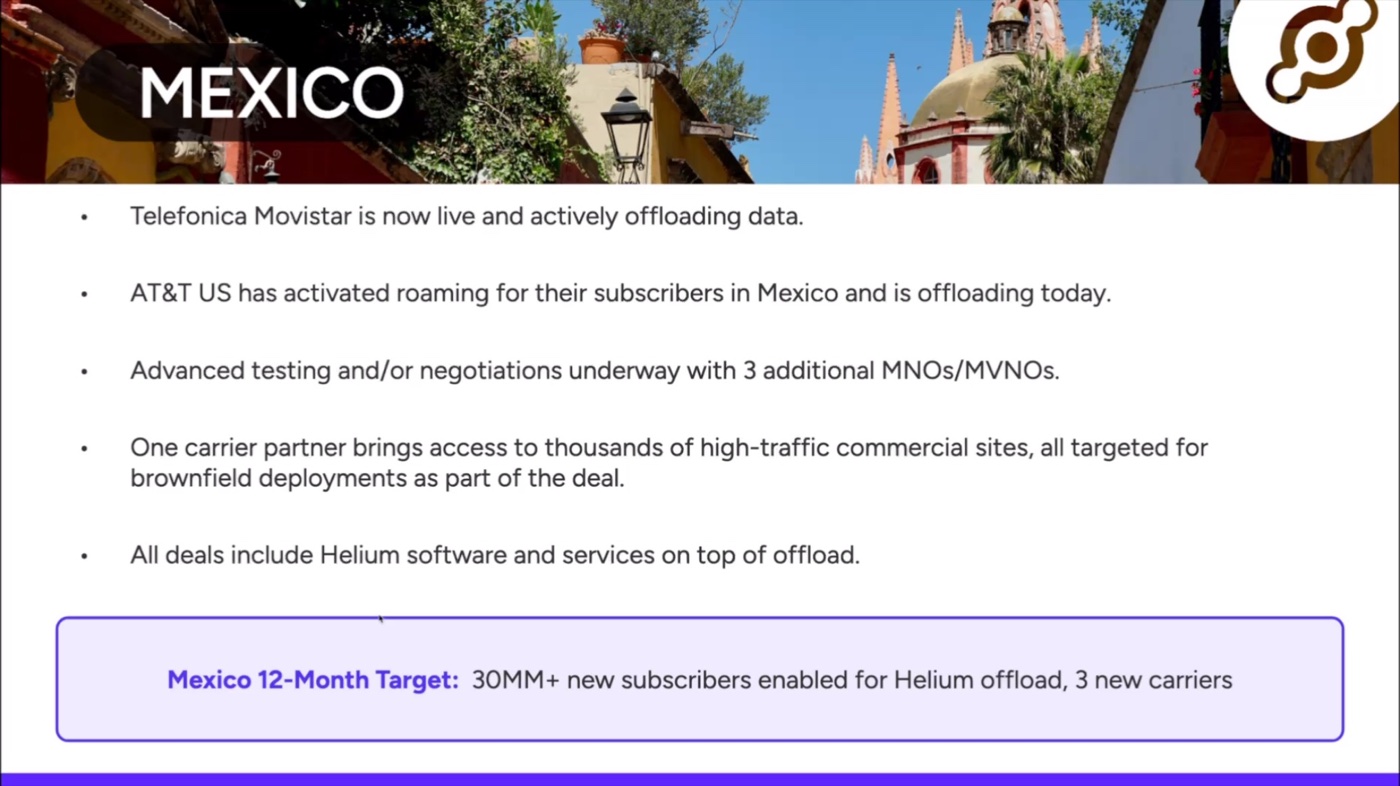

For Mexico, the team said Telefonica Movistar is live and actively offloading, AT&T US has activated roaming for subscribers in Mexico, and three additional MNOs or MVNOs are in advanced testing or negotiations. The Mexico 12-month target was 30M+ new subscribers enabled for Helium offload and three new carriers.

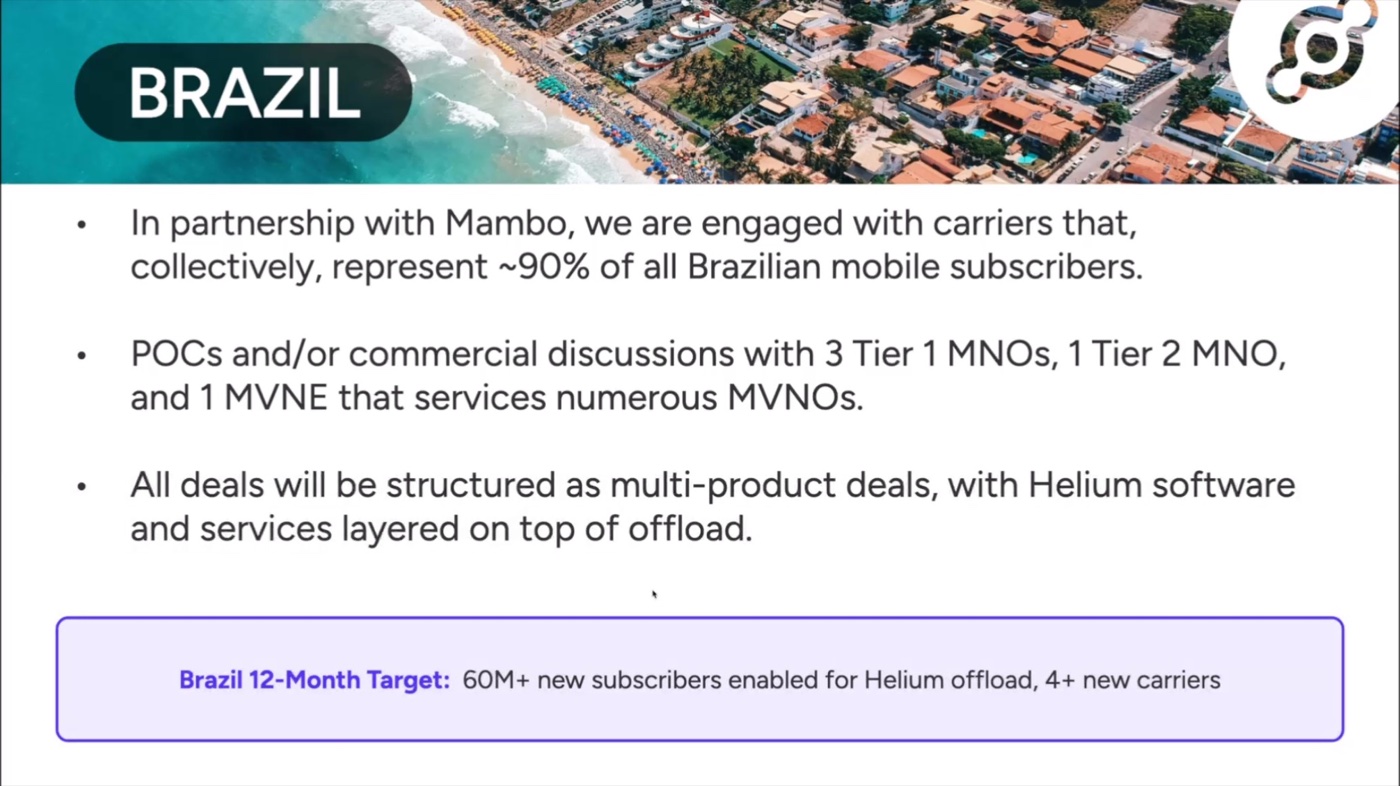

For Brazil, the team highlighted a partnership with Mambo. The slides said Helium is engaged with carriers that collectively represent about 90 percent of Brazilian mobile subscribers, with POCs or commercial discussions involving three Tier 1 MNOs, one Tier 2 MNO, and one MVNE. The Brazil 12-month target was 60M+ new subscribers enabled for Helium offload and 4+ new carriers.

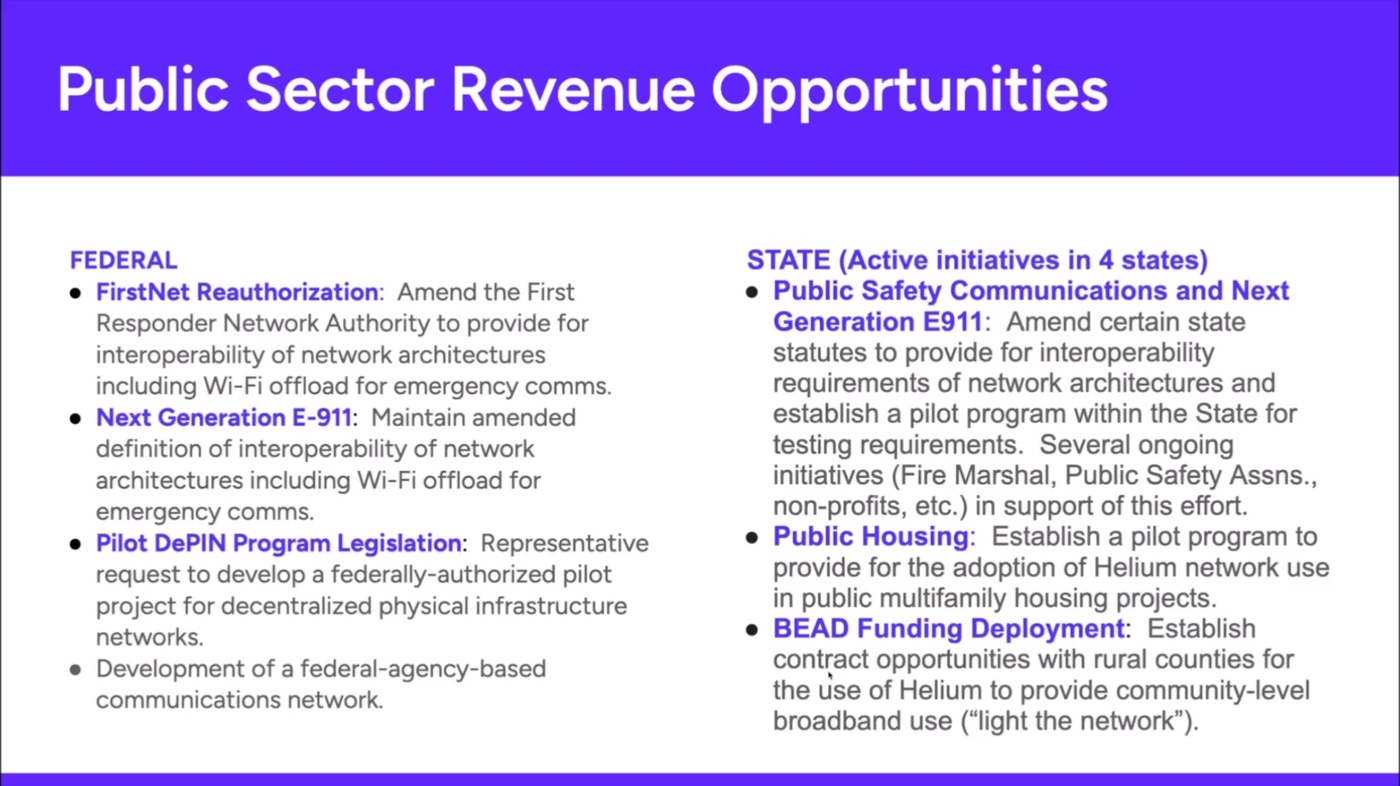

Public-Sector Opportunities

The presentation also covered public-sector revenue opportunities. Mario described work at the federal and state levels to promote interoperability requirements that include Wi-Fi offload, especially for first responders, emergency communications, and agency programs. The slide deck mentioned FirstNet reauthorization, Next Generation E-911, state pilot programs, public housing, and BEAD-related rural broadband opportunities. These were presented as active opportunity areas, not as closed revenue.

Community Q&A

The first Q&A topic was whether stalled visible user and data metrics meant carriers were curtailing offload. Mario said no, arguing that the issue was mostly lack of useful expansion and activation timing. He said greenfield traffic had declined while brownfield traffic was up, and that signed brownfield deals can take time to activate and show up in usage.

Several questions focused on transparency. Mario said Nova would not publicly disclose payroll, individual compensation, or full private-company financials, but that the proposed council should receive summary financials and other privileged information under appropriate restrictions. He said the council is meant to help evaluate resource use, KPIs, and whether distributions match the proposal's purpose.

On whether protocol resources should create community equity in Nova, Mario said the proposed HNT emission is not an equity investment in Nova. He described it as protocol-level resources deposited into a vault for network operations and growth, with Nova administering the program under oversight. He argued that giving a DAO equity in Nova would blur protocol governance and corporate governance and create legal and practical problems.

On network operating costs, Mario said the company uses AWS for many services and gave an approximate monthly operating-cost range around $120k, while noting that the team has been reducing those costs over time. He used that answer to emphasize that a network serving millions of users needs ongoing infrastructure resources.

On offload rates and secondary revenue, Mario said near-term US offload rates can be very low, but that carriers pay a range of rates and that some international markets may have stronger economics. He described quality-of-service gateways and other carrier tools as secondary revenue streams that open telco conversations, while still depending on the Helium Network as the underlying offload footprint.

On international expansion, the team argued that the US remains central, but some markets may feel the carrier-capacity pressure sooner. Mexico required more early infrastructure work, while Brazil is being approached through Mambo so that local footprint and business-development relationships exist from day zero. The team said future geographies need strong local partners and carrier readiness.

The final Q&A question asked whether the proposed inflation event could be programmatically locked so HNT is permanently capped afterward. Mario said no governance lock can be made truly permanent because a future vote could change it. He said he would not promise a permanent cap, while also saying that any future change would require governance.

Presentation Slides

The town hall included a slide deck covering the carrier demand thesis, product roadmap, brownfield pipeline, expansion targets, and public-sector opportunities.

01. Global Pressures

01. Global Pressures

02. 5G and 6G Costs

02. 5G and 6G Costs

03. Satellite Coverage

03. Satellite Coverage

04. Indoor Demand

04. Indoor Demand

05. Capacity Crunch

05. Capacity Crunch

06. Fixed Wireless

06. Fixed Wireless

07. Proof Today

07. Proof Today

08. Real Economics

08. Real Economics

09. Tech Roadmap

09. Tech Roadmap

10. Deployer Tooling

10. Deployer Tooling

11. Brownfield Expansion

11. Brownfield Expansion

12. Brownfield Pipeline

12. Brownfield Pipeline

13. Carrier Pipeline

13. Carrier Pipeline

14. US Market

14. US Market

15. Mexico Market

15. Mexico Market

16. Brazil Market

16. Brazil Market

17. 12 Month Expansion

17. 12 Month Expansion

18. Public Sector

18. Public Sector

Numbers and Claims to Track

- US carrier request: about 30,000 locations for Helium coverage.

- AT&T: about 2M users connecting to the Helium Network daily, according to the presentation.

- T-Mobile: approaching about 1M daily active users, according to the presentation.

- Brownfield growth: 5,806 access points added in May, with 15,324 brownfield units in the pipeline snapshot.

- 12-month expansion case: 8+ new carrier or partner relationships and 105M+ new subscribers enabled for Helium offload across the US, Mexico, and Brazil.

- Brazil market: carriers in discussion were said to collectively represent about 90 percent of Brazilian mobile subscribers.

- Governance: advisory council candidates are expected to receive more guidance before the vote.

Key Themes

- Helium's carrier strategy is being framed around indoor Wi-Fi offload, not only hotspot count.

- The team sees brownfield venue coverage as more resilient than purely greenfield deployment.

- Carrier enablement products are intended to make Helium more than a raw offload network.

- The proposal asks the community to fund network growth through protocol resources rather than Nova equity.

- Transparency will rely on a council structure because the team says some commercial and financial details cannot be public.

- The strongest community tension remains trust: whether new resources will turn into durable carrier revenue and deployer earnings.

Open Questions and Follow-Ups

- How quickly the 30,000 US expansion-zone locations become live, useful coverage and visible usage.

- How much of the 105M+ subscriber-enabled bull case converts into actual recurring offload traffic and revenue.

- What carrier rates, margins, and quality-of-service revenue look like as markets move beyond subsidized growth.

- How the advisory council will be selected, what legal requirements council members must meet, and what information it can disclose publicly.

- Which public-sector initiatives become pilots, contracts, or formal requirements rather than opportunity areas.

- Whether the network can grow traffic enough for the proposed inflation to look small relative to future usage and burn revenue.

- How deployer financing, leasing, or subsidy ideas develop, especially for operators who cannot rely on existing brownfield infrastructure.

- How future governance handles emissions once the proposed schedule is complete.

Sources

- Original recording: Public Discord town hall recording.

- Presentation materials: Slides shown during the Discord town hall.

- HIP 149 proposal text: https://github.com/helium/HIP/blob/main/0149-helium-utility-and-emissions-realignment.md

- Official proposal: https://www.helium.com/proposal

- Helium blog post: https://blog.helium.com/the-next-era-dbd0b4dd4939

- Transcript: transcript.txt

- Related event: Helium Proposal Discussion Q&A

- Related announcement: Helium Network Proposal Announcement

These notes and the transcript were prepared with AI assistance. Source materials are linked for verification.